- The Wealth Expedition

- Posts

- Can You Still Make Money in Real Estate in 2025?

Can You Still Make Money in Real Estate in 2025?

Is real estate still a smart investment in 2025? Discover the surprising truth and what it means for your wealth.

Daniel Lancaster

August 30, 2025

In partnership with

Good morning!

A LOT is happening over here at the Wealth Expedition!

Many people start with nothing — no savings, no income, no idea where to begin.

That’s exactly why this upcoming membership includes a comprehensive course designed to take you from ground zero to financial abundance in the right order. You won’t just learn how to budget in isolation or how to invest without context. Each lesson stacks on the last, creating a clear, step-by-step path to transforming your entire financial life.

And here’s the best part: it’s not just a course, it’s an epic adventure.

Every budgeting breakthrough, investment decision, or entrepreneurial step is woven into a larger story — your story. You’ll step into the role of hero, with me as your guide—advancing through fantastical realms, unlocking achievements, keeping streaks alive, and watching real-world financial wins stack up right alongside your in-course progress.

The weekly newsletter gives you insights and deep dives you can apply whenever you like. But this course? It pulls you forward with accountability, structure, and momentum — so you always know your next step.

I seriously cannot wait to share this with you all. You are an AWESOME tribe — and we’re about to embark on an adventure like no other!

Quick question: where are you on your wealth expedition?

1️⃣ Just starting out

2️⃣ Making progress, but want more

3️⃣ Crushing it and ready to level up

Bonus: what’s your biggest financial frustration or goal right now?

Hit reply—I read every response, and your feedback will shape the course and future newsletter content.

I’d love to hear from you.

Keep up the great work!

Daniel

100 Genius Side Hustle Ideas

Don't wait. Sign up for The Hustle to unlock our side hustle database. Unlike generic "start a blog" advice, we've curated 100 actual business ideas with real earning potential, startup costs, and time requirements. Join 1.5M professionals getting smarter about business daily and launch your next money-making venture.

📽️ If you prefer to watch instead of read, I’ve also covered this topic in a short YouTube video—check it out here.

FINANCIAL TOOL

Can You Still Make Money in Real Estate in 2025?

When it comes to accelerating wealth accumulation, three primary vehicles can carry us up the mountain:

Capital markets — stocks, bonds, and alternatives.

Long-term average annual return of the S&P 500: ~9–10%.

Real estate — residential and commercial property.

Residential real estate (20-year average): ~3.1%.

Commercial real estate (20-year average): ~6.5%.

Business ownership — startups, acquisitions, and franchises.

For established businesses (franchises, acquisitions), long-term returns typically fall in the 5–20% range.

Startups are far more volatile: many fail entirely, while a few deliver outsized returns that can dwarf averages, sometimes 50% or more annually.

At first glance, real estate seems like the slowest path. But real estate plays by a different set of rules.

What Makes Real Estate Different?

Unlike stocks or businesses, the value of real estate is:

Anchored in physical property — not intangible factors like brand, goodwill, organizational efficiency, supplier relationships or company culture.

Highly leverageable — you can control a large asset with a relatively small amount of your own money.

Tied to interest rates — long-term borrowing costs shape both prices and profitability.

Influenced by economic cycles — especially supply and demand for housing and mortgage loans.

The true “superpower” of real estate lies in its combination of tangible value and leverage.

Think about it: a home’s practical use today is almost the same as it will be in 20 years. Unlike a company that can become obsolete, the shelter value of a property remains constant. This stability is one reason real estate is often less volatile than the stock market.

But add leverage, and the math changes dramatically.

How Leverage Amplifies Returns (and Risks)

Imagine buying a $200,000 property with a 20% down payment ($40,000). If housing prices rise just 3% annually, your return on invested capital can jump to 15% because of leverage (ignoring transaction costs and mortgage principal repayment).

Sounds great — but here’s the catch.

If property values fall 5%, the actual value of your investment (your equity) falls 25%. Similarly, an 11% rise in value translates to a 55% return.

Leverage magnifies outcomes. With it, real estate can outperform stocks — but it can also underperform them by a wide margin.

How Wild Can Housing Prices Get?

When we talk about the stock market, most people understand the idea of volatility—prices can swing up or down, sometimes by huge amounts. Housing, on the other hand, feels more stable. But how stable is it, really?

Economists have tried to measure this using something called the standard deviation from trend. That’s just a fancy way of saying: “How far do prices usually wander away from their long-term path?”

Here’s what the research found:

Across many countries, the typical amount prices wander from trend is about 15%.

In plain English: even a 20% swing in house prices isn’t unusual for a given year.

Go out three standard deviations, and you’re talking about nearly 50% price moves compared to trend.

The U.S. has historically been on the lower end of volatility, with about 8% standard deviation. This doesn’t mean housing always moves ±8% each year — it’s an average spread from the long-term trend.

Japan, on the other hand, has seen wild swings—closer to 48%, with France at 25%. Imagine what that volatility does for an investor that’s using leverage!

Two caveats:

Don’t forget: standard deviation of housing prices can vary dramatically even within the same country. Phoenix and San Francisco can be worlds apart on their housing prices, for example.

One big asset bubble event can dramatically change the standard deviation. It’s important to look at the long-term trend like this, but also to look at shorter term trends of what’s happened is more recent history (10-20 years, for example).

So what’s the takeaway? Housing isn’t immune to volatility. While it doesn’t whiplash like tech stocks, it does swing—sometimes hard. This is a good reminder not to assume that real estate always goes up in a smooth line.

Instead, think of housing as an asset that can experience cycles, bubbles, and corrections—and plan your financial strategy with that in mind.

Does It Still Make Sense to Buy Real Estate Today?

Median U.S. home prices are now about 5.3x higher than median household income (2023). For context, that ratio was just 3.2x in 1970. So the affordability challenge is real.

Much of this doesn’t appear to be a classic housing bubble—it’s more about supply and demand imbalances:

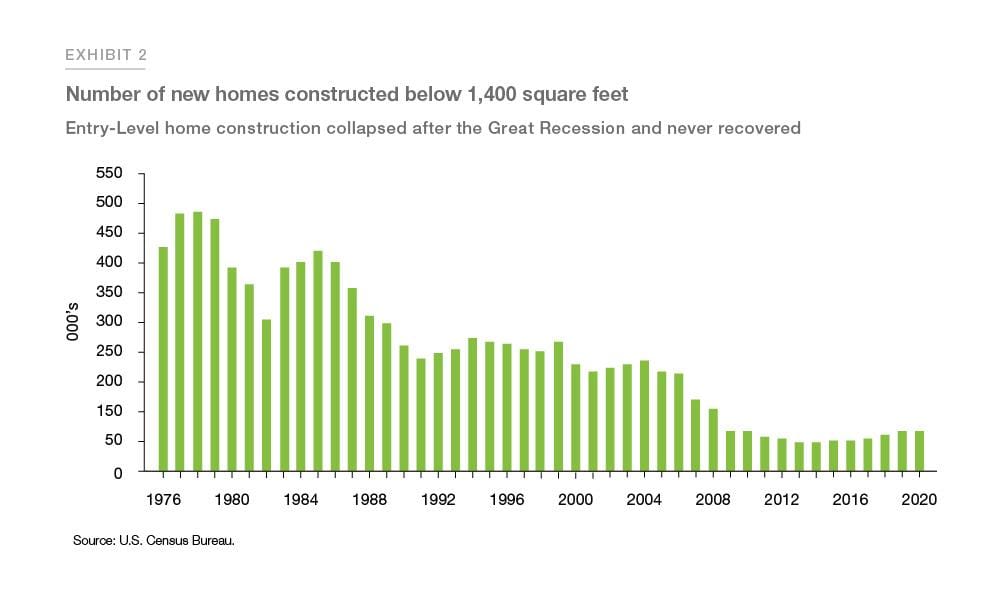

Fewer entry-level single-family homes are being built (think 1,400 sq. ft. or smaller).

Construction costs have soared, partly due to supply chain disruptions during the 2020 economic shutdowns.

Higher interest rates discourage existing homeowners from selling, keeping inventory tight.

Despite the challenges, real estate can make sense if approached strategically.

Let’s look at three types of investors:

Investor A: Puts 20% down on an investment property. To balance the added risk of leverage, he ensures his stock portfolio is at least equal in value to the property’s mortgage balance.

Investor B: Puts 50% down. She aims for an equal amount invested elsewhere for diversification.

Investor C: Buys 100% in cash. Diversification still matters, but the proper amount depends largely on her liquidity needs and risk appetite.

In other words, if an investor is going to use leverage on real estate as an investment (it’s different if you’re buying it for personal use), then they should also make sure they have an amount equal to the mortgage balance diversified in other investments, such as the stock market.

Regardless of approach, each investor keeps an emergency fund with 3–6 months of living expenses plus housing costs (including the mortgage payment).

What to Expect Looking Ahead

Forecasts suggest U.S. home prices are estimated to grow 2%–3.4% annually through 2030.

Modest on its own. But once you add net rental income and leverage, the potential returns can become quite meaningful.

Of course, forecasts are never guarantees, but they help to anchor expectations.

The bottom line: real estate can be a powerful accelerator of wealth, but only when placed in the right context — as part of a diversified portfolio, with careful attention to risk, liquidity, and leverage.

Real estate can also be a great diversifier. Even when leveraged and volatile, real estate often moves independently of the stock market, meaning it may be doing one thing while stocks do another. This mix of asset types can create a healthier overall risk/return profile, even with inherent volatility.

Action Step: Run Your “Leverage Test”

If you’re considering real estate as an investment, don’t just ask, “Can I afford this property?” Instead, ask:

How much leverage am I using? (10% down? 20%? 50%? 100% cash?)

How does that leverage amplify both my potential gains AND losses?

Do I have at least an amount equal to the mortgage invested elsewhere to diversify my risk?

Put these numbers on paper. If a 5% drop in property value means a 25% drop in your investment, are you prepared for that? If the answer is no, adjust your leverage or save a bit more in a diversified portfolio before you buy.

By running this simple test, you’ll approach real estate with clarity, confidence, and a plan that aligns with your overall wealth expedition.

Disclaimer

This newsletter is for educational and informational purposes only. It does not constitute personalized investment advice, financial planning, legal, or tax advice. The views expressed are general in nature and should not be relied upon for making individual financial decisions. Always consider your personal circumstances and consult with a qualified professional before making investment choices.

How did you like today's newsletter?I'm always looking for ways to offer greater value to fellow explorers. Your feedback helps set the direction for future content! |

I’d love to hear from you. Let me know what you’d like to see in upcoming newsletters, articles, or a digital course at Contact Us - The Wealth Expedition.