- The Wealth Expedition

- Posts

- Future of Reserve Currencies

Future of Reserve Currencies

What is the relationship between the US national debt and the country's ability to maintain its global position of power? Two CFA Charterholders offer insights and guidance for steps the US needs to take.

Daniel Lancaster

February 10, 2025

Our weekly newsletter features the following sections:

First time reading? Subscribe for weekly content here.

“[Alexander Hamilton, Secretary of the Treasury] ardently wishes to see it incorporated, as a fundamental maxim in the system of public credit of the United States, that the creation of debt should always be accompanied with the means of extinguishment. This he regards as the true secret for rendering public credit immortal.”

-Alexander Hamilton in The First Report on Public Credit (1790)

NEWS

What Happened Last Week

According to a new Gallup poll, Americans are the most optimistic they’ve been in the past seven years about economic growth, stock market growth, interest rate drops and slowing inflation.

This year, 8% of companies have lowered future performance estimates, while 5% have raised them.

The US economy added 143,000 jobs in January, just below expectations.

Unemployment improved by falling to 4% (an eight-month low) while wage growth remained healthy.

November and December’s job gains were revised significantly upward, which led to Treasury interest rates climbing higher.

Proposed tariffs on Canada and Mexico have been postponed due to each respective country’s declared willingness to make a concerted effort against the flow of fentanyl and illegal border crossings.

How I See It

Remember the utter pessimism that reigned supreme in 2022?

That pessimism is long gone. And if anyone had sold out of the markets in October 2022 when things looked bleak, they would have missed out on 46% positive upside since then.

Pessimism is a good thing for markets. Optimism can be a good thing too, but only what I’ll call vigilant optimism. A sort of optimism that stays cautious and doesn’t overlook negative developing trends.

Optimism can continue on for years. And it often drives some of the stock markets best returns.

What I like to see is that companies are setting lower expectations. Lower expectations give room for positive surprise. Markets move on the difference between expectations and reality.

Other positive developments include the healthy continuation of the jobs market, expectations of higher interest rates for longer, and the possible avoidance of tariffs with our neighbors.

Here are a few reasons why I think markets will end the year positive: declining uncertainty, fewer tariffs than expected, lower impact of tariffs than expected, and a loosened regulatory environment which drives faster innovation.

That said, the first two years of a President’s term have historically been the most likely for bear markets to develop. There are reasons for that, mainly due to the fact that they usually have greater potential to effect dramatic changes during those initial years.

The myriad changes happening presently are difficult to calculate in their combined outcomes, but the present optimism among small businesses and US residents seems to indicate a shared belief that the streamlining of American government and business is likely to pay off, in the end.

PARADIGM SHIFT

Future of Reserve Currencies

The US dollar has been the global reserve currency since the end of WWII.

That means countries around the world hold US Treasuries in reserve, allowing them the capability to strategically buy and sell their own currencies as they attempt to maintain stability of value.

As deglobalization has gained some momentum around the world, could there come a time when world trade is divided into two or more BLOCs?

That is, could countries begin favoring trade with one another to the partial or total exclusion of outsiders?

And if so, would the US dollar be at risk of losing its global reserve status?

Oliver Fines, CFA, and Mark Higgins, CFA, tackle this question in a recent podcast.

In their opinion, the US became the world reserve currency largely due to the dollar’s convertibility to gold in 1944.

Even though the gold reserve was eventually removed, there has never since been a better alternative for the reserve currency, as the momentum of the US’ economic power continues to build upon itself.

Because US Treasuries are in such high demand, some speculate this allows the US government to borrow at lower interest rates than might otherwise be possible. But without the backing of gold, what prevents the US dollar from declining in popularity against, say, the euro or even cryptocurrency?

The perception of the US dollar’s strength is largely tied to its perceived ability to make good on its payments sustainably (without harming its economy), and that means a prudent handling of national debt.

Alexander Hamilton insisted upon the following two principles for public debt:

A nation needs sound credit in order to fund the response to public danger when it arises.

The public credit should be paid back once the danger subsides.

And the US roughly followed this guidance up until its dollar became the world reserve currency after WWII.

But we became too comfortable, growing the national debt from about $200 billion at Bretton Woods (1944) to over $36 trillion today.

The point that Olivier and Mark make is that the US deficit levels are not sustainable. If they continue this way for another couple of decades, there will need to be a massive cut (20%+) in US spending, which will largely include programs which US citizens have come to depend on and plan around.

The better option, in their opinion, is to make smaller changes now which will minimize the pain necessary to make things sustainable.

There is a strong necessity to restructure the US budget, which is currently being examined by DOGE. Although it won’t be easy, a successful budget restructure could help solidify the US dollar as the only viable world reserve currency for decades to come.

The possible end of the dollar’s reserve status wouldn’t likely spell disaster for the US economy (it’s much less important than many assume), but taking steps to strengthen our long-term economic sustainability is one positive development that’s long overdue.

FINANCIAL TOOL

Investment Grade Bonds

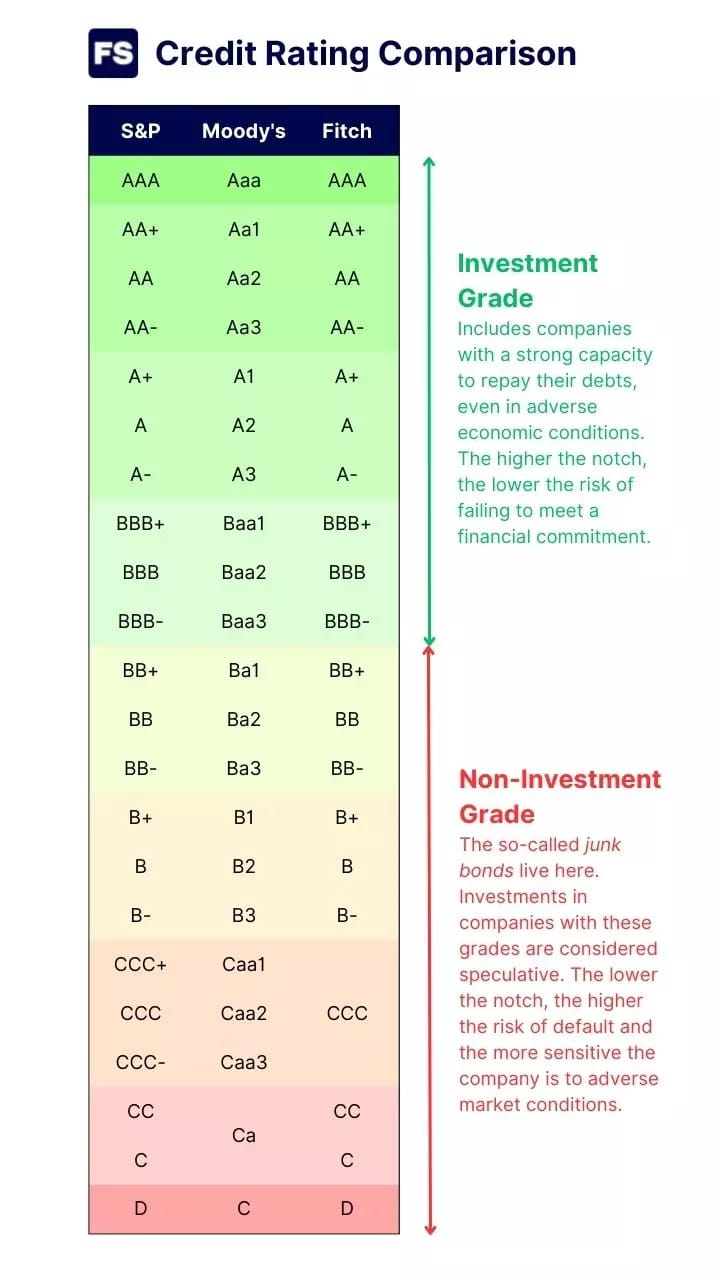

There are three main bond rating agencies in the US: Standard & Poor’s, Moody’s, and Fitch Ratings.

They evaluate the capability of a government or corporation to make its interest and principal payments as per the original bond contract.

While there are several tiers that a bond can be rated, it’s simplest to think in terms of investment grade versus junk bonds.

It’s important to understand the difference between these two types!

The first reason bonds are included in any portfolio is to capture a better than cash return while keeping volatility lower than stock.

The second reason is that bond values move largely independently of stock values, and this low correlation enhances diversification and reduces overall risk based on any one economic driver.

But here’s the thing: these two reasons apply mainly to investment grade bonds. That is, they apply to bonds which are highly unlikely to default.

US Treasuries are generally considered the safest bonds that can be purchased, because of the power to tax and borrow almost without limit. Corporate bonds of strong companies are next in line, but because of the additional risk (no power to tax, limited power to borrow), investors demand a slightly higher interest rates above the US Treasury rates.

Investment grade bonds are especially important for short- and intermediate-term investors. Anyone looking to invest for 10 years or less before needing access to a significant portion of their funds would likely benefit from holding 30%-100% in investment grade bonds. The exact amount depends on their goals, flexibility and personal risk aversion.

While I’ll cover junk bonds separately, suffice it to say here that their enticingly high interest rates are not as attractive as they first might appear. For anyone needing largely predictable returns (say if they’re saving for a house or other large purchase), junk bonds are not ideal.

For most investors, bond ETFs are a great option for achieving diversity and liquidity. Some junk bonds are usually included in any bond ETF, but those who wish to limit their risk should aim for exposure of 10% or less.

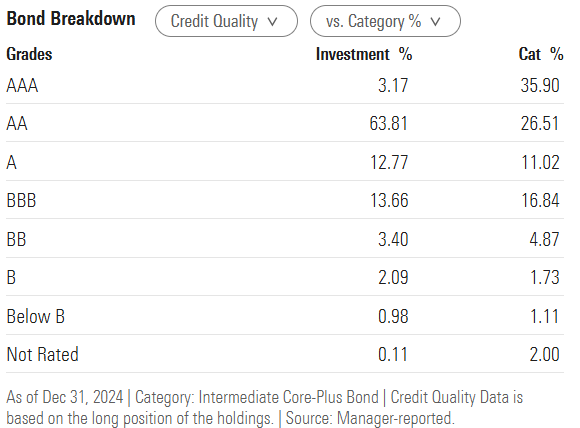

Morningstar.com offers an excellent breakdown of bond quality within an ETF under their Portfolio tab.

For example, Morningstar shows the following breakdown for iShares Core Total USD Bond Market ETF (IUSB):

*Investment % describes the make-up of the ETF. This is compared with the average constitution of others in its category.

And finally, as a guide to the ratings, this graph from Financestu.com shows the three rating systems and what constitutes investment grade:

HERE’S HOW I CAN HELP

COURSE 2 OF 3 IS AVAILABLE!

I am in the process of creating the third and final in-depth digital course that, together with the other two, will comprehensively make you a master of your financial destiny.

The second of three courses is now available:

This course will lead you step-by-step toward developing your escape plan into a life of comprehensive wealth: time, flexibility, purpose and money.

Walk through the lessons and accompanying action steps to create an extraordinary life change today which culminates in a bridge to financial independence in the near future.

Each lesson builds upon the last, covering these main topics:

Master high-impact budgeting techniques to create a surplus today

Develop a plan to become debt-free in record time

Raise your salary this year

Use tax strategy to fast-track your goals

Bridge your way to entrepreneurship

This is a learn-at-your-own-pace course with 7+ hours of content that will set you on course to achieve your dream life well in advance of retirement age using simple but powerful habits of finance.

I’d love to hear from you. Let me know what you’d like to see in upcoming newsletters, articles, or a digital course at Contact Us - The Wealth Expedition.