- The Wealth Expedition

- Posts

- How Much Risk Do You Want?

How Much Risk Do You Want?

When media starts talking about WWIII, are you ready to hold your nerve in the markets? Here's one way to manage risk.

Daniel Lancaster

November 25, 2024

Our weekly newsletter features the following sections:

First time reading? Subscribe for weekly content here.

“Don't risk what is important to you, to get what is not important to you.”

-Warren Buffett

NEWS

What Happened Last Week

Russia fired intermediate-range ballistic missiles at Ukraine on Thursday in response to Ukrainian long-range strikes inside Russian territory using US and UK-made missiles.

Housing starts dropped 3.1%, but housing completion is still happening more rapidly than a year ago. That means the number of houses under construction is declining.

The Leading Economic Index (LEI) dropped below 100 to 99.5 for November, which is generally viewed as a sign of future economic slowdown.

The Services Purchasing Managers Index (PMI) rose to 57, well above estimates for November, marking the fastest expansion in the services sector since March 2022.

The Manufacturing Purchasing Managers Index (PMI) rose in line with estimates to 48.8, which still indicates slowdown in the goods industry but not slowing as much as during the last three months.

Investor sentiment is cautiously optimistic, but an above average 33.2% of investors expect a bear market over the next six months. Mixed messages appear to show a positive outlook, though the short-term market forecast is divided, according to the AAII Investor Sentiment Survey and Fear and Greed Index.

How I See It

Markets almost never do what the majority expect. That’s the main thing I look for in these weekly new reports.

It’s no question that some pessimism has made investors anxious this past week, especially surrounding the renewed talk around Russia’s intentions and capabilities.

Markets can do anything in the short-term. By short-term, I mean anything less than one year. But successful investing is all about optimizing returns within the targeted timeframe.

So we don’t try to jump out of markets for a downward move that lasts a few months. That’s a losing game, and an unnecessary one to play. So long as we’re back where we were without losing a year’s time or more, it is statistically better to get used to riding through those pullbacks and corrections.

There are things we can do to protect against big downside risk, which I’ll touch on soon, but here let’s examine what markets expect.

Bear markets usually begin slowly. They hit a peak and taper off like a rolling hill, while the majority voices continue to say, “Now’s the time to buy more!”

I don’t see that happening at the moment.

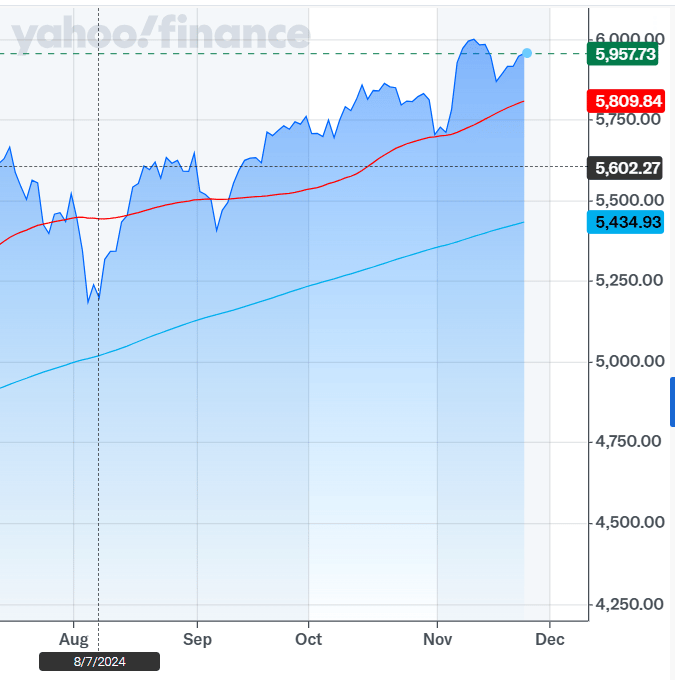

The chart below shows the S&P 500 over the last five months, along with the 50- and 200-day moving averages (red and blue lines respectively). This trend, for now, is still clearly positive.

Source: Yahoo Finance

Of course, that can change, and we’ll continue to keep close eyes on that.

But while sentiment has been hit recently by political and geopolitical uncertainty, there remain signs of healthy underlying growth.

First years of a President’s term tend to be lackluster, but often better when it’s the first year of a second term.

Markets don’t need huge political wins or other economic boons to have a good, positive year. They just need reasonable sentiment and positive growth in an economy. Both of these appear to be present in today’s America.

PARADIGM SHIFT

How Much Risk Do You Want?

Since the election of President Donald Trump, the news has been rife with speculations over what that means for the markets.

Markets like predictability. It’s why they often favor a balance of opposing ideas among Congress, and between the Congress and the President.

But while some uncertainty has declined (we know who our next President will be), there still remains a lot of uncertainty as to the net effect of all proposed changes.

Markets love the idea of cutting regulations. That is a tailwind to growth.

Other outcomes are not so clear cut.

For example, what happens to GDP if $2 trillion of government spending is no longer being paid to employees, contractors or other businesses for goods and services? Will the cut in regulations and taxes be enough to counterbalance that drop in GDP by fueling the needed economic growth in the private sector?

And what about tariffs on China? While this adds the risk of further above-average inflation, it reduces the risk of international dependence (at least on a potential world superpower).

In the midst of all this we have AI, which is still a question of just how much it is going to improve efficiency per worker (and thus lower long-term cost) in the economy in the years ahead.

Markets are trying to juggle and analyze all of these things and more.

The fact is, the one thing we can be sure of is that investors are hyper aware of this uncertainty. And that’s a great thing! As that uncertainty fades in the midst of a neutral/optimistic outlook, that gives markets fuel to trend upward.

The moment we want to watch for is when markets appear to hit a peak and trend sideways to slightly down over about three months. This is how most bear markets begin. Right now, we’re not seeing that, but it’s something we should be aware of.

Those who wish to limit the downside in their portfolios might be interested in securing insurance against a market drop. How does that happen? With the use of a put option.

You can specify how much you’re willing to risk, and how much you’re willing to give up in potential rewards. Read the next section to learn more!

FINANCIAL TOOL

Put Option

Did you know you can buy insurance against market downside?

That’s right. It’s expensive. But in certain cases I believe it’s very much worth it.

A put option is exactly that.

It gives you the option to sell your shares at a pre-agreed price called the “strike price.”

Imagine you own a stock index called XYZ, and it’s priced at $100.

Maybe you’re bullish but you don’t want to risk any more downside than 15%. What could you do?

You could buy a put option on XYZ shares with a strike price of $85. That means even if your shares drop below $85, you can still sell the shares for at least $85.

Note that options have an expiry date. But you can buy options for a long time. You can buy them for a year or longer if you want.

Here’s the thing about options: every option covers 100 shares of a stock or ETF. So if you own 500 shares of XYZ, you would buy 5 options of XYZ to cover the full downside beyond 15%.

Options are going to vary in price depending on several factors. But to give you an idea, buying a put option for one year with a strike price set at 15% below the current price might cost you somewhere around 2-3% of the portfolio position you’re protecting.

Expensive right?

But think of it this way. If there is a reason why you can’t afford to lose more than 15%, then it may be worth the cost.

These reasons could include needing a large chunk of the money within the next few years, for one reason or another.

Or it may be a way of keeping you from otherwise trying to jump out of markets in volatile times.

Assume XYZ has the following returns over five years: 20%, 0%, -25%, 35%, 28%.

That’s an average of about 9.23% compounded annually.

If you held a put option that cost you 3% and protected beyond a 15% drop, then your net profits would have been something like: 16%, -3%, -15%, 31%, 24%.

That’s an average of about 9.21% compounded annually.

In this example, the final results are nearly neck and neck. But here’s the important difference. If the investor needed to protect the money beyond a certain drop in the short-term, then the put option strategy was worthwhile.

Because in the midst of the bear market, the put option strategy allowed the total portfolio to retain higher value during the worst parts of the downside.

And if the investor needed to make a quick withdrawal during that time, they wouldn’t be withdrawing from such a low-valued portfolio.

There are other strategies you can perform with options, but this perhaps is the simplest. And it can be powerful for certain short- and medium-term goals!

HERE’S HOW I CAN HELP

Course 1 of 3 is Available for Enrollment!

I am in the process of creating a total of three in-depth digital courses that comprehensively will make you a master of your financial destiny.

The first course, called Low Risk Investing, is available now and ready for enrollment. This lays a solid foundation for risk management and everything else investing.

Understanding and utilizing these strategies will give you confidence in knowing exactly what risk to take and why. It will also show you how to eliminate the unnecessary and unwanted risks while maintaining great potential for returns.

These are pre-recorded courses that you can follow at your own pace.

What you’ll get with over 3.5 hours of content:

Learn to identify the main risks of investing.

Discover the financial tools, products and strategies at your fingertips.

Determine the risk factors you want to reduce.

Learn how to build a diversified portfolio that weights the odds of success heavily in your favor!

Access a risk tolerance questionnaire, a quick guide to low risk investments, a list of scenarios paired with low risk portfolios, and a list of companies where you can access such strategies.

I’d love to hear from you. Let me know what you’d like to see in upcoming newsletters, articles, or a digital course at Contact Us - The Wealth Expedition.