- The Wealth Expedition

- Posts

- The Fed's Secret Weapon

The Fed's Secret Weapon

Can the Fed save us from recession? Or is it up to us?

Daniel Lancaster

May 03, 2025

Good morning!

While I’m making my way home from visiting St Augustine, Florida, I’m reminiscing on the Spanish explorer who first set foot there and claimed “La Florida” for the Spanish Crown. Talk about an expedition! Ponce de Leon led the first European expedition to this now beloved coastal state. He may not have discovered the fountain of youth, but he discovered a coastal paradise that makes us all feel young at heart!

Just goes to show that when we take a risk, and we set out on an expedition to transform our lives, there’s no guarantee and no perfect way to know exactly what the end result will look like. But we know this: we will be changed. Regardless of the material things, when we take control of our destiny, sink or swim, we will grow and mature. We allow the path to change as we pass through each milestone, correcting course as we learn. And in the end, if we don’t give up, the earth and all that’s in it will be ours to enjoy.

While the fountain of youth may remain a myth, our personal wealth expedition can lead to something richer: reclaiming our time now and spending our lives in more meaningful ways.

This week’s newsletter includes:

What Happened This Week

The Fed’s Secret Weapon

Treasury Inflation Protected Securities (TIPS)

Launch Your Personal Wealth Expedition!

Be sure to check out this week’s YouTube video continuing the subject of sustainable and meaningful budgeting.

NEWS

What Happened This Week

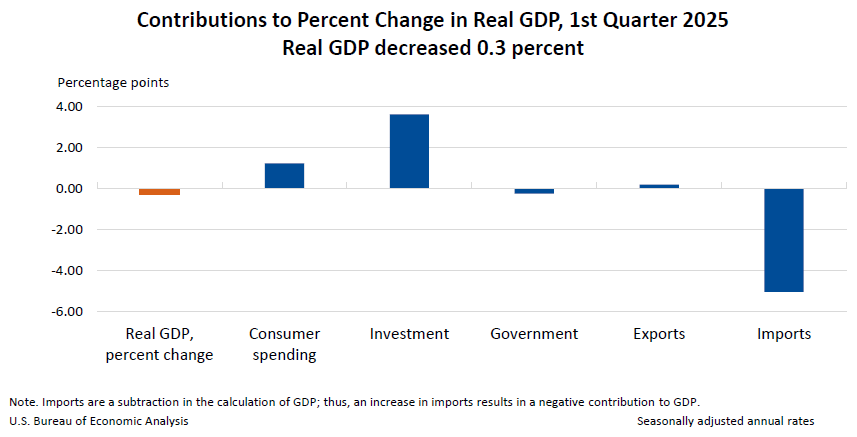

US Real GDP declined by -0.3% in the first quarter of 2025.

This decrease was largely caused by an increase in imports (which is a negative in the GDP equation) and decrease in government spending.

There were increases in exports, investment and consumer spending.

The Personal Consumption Index (PCE) increased an annualized 3.6% in Q1, an acceleration in inflation since last quarter’s 2.4%.

Source: Bureau of Economic Analysis

The US Manufacturing PMI improved to 50.7 in April, well above expectations.

The US Services PMI dropped below expectations, however, to 51.4.

PMI numbers above 50 suggest a growing economy, but business confidence and output sentiment dropped due to continued uncertainty.

How I See It

Last week, I mentioned that we’d likely hit resistance around $5,689 for the S&P 500.

This week, the S&P 500 had a great week, touched $5,700, but closed just below at $5,686.67, meeting that slight resistance I forecasted.

It’s become clear that the US government is likely to continue making changes that keep uncertainty high. The good news is that investment improved last quarter, and the dramatic increase in imports is not likely to repeat itself in the second quarter.

The Fed is in a difficult place, because if they keep interest rates steady, this could push markets lower which may be more difficult this time to recover from. If they lower interest rates, they risk adding fuel to an already accelerated inflation rate.

Which one is most important in order to avoid recession?

In my opinion, two things need to happen.

I think the Fed needs to focus on unemployment more than inflation right now, which means lowering the interest rate by 25 bps (0.25%) in May.

I think the Federal government needs to make quick work of their economic plan, announcing the specifics of any planned tax cuts, along with any other major sweeping changes. Get it all out now so that uncertainty can only decrease from this point.

We’ll know if point 1 happens next week.

The good news right now is that, despite sentiment falling, there still remains potential for continued growth, even renewed strength, if the government and the Fed can remove some uncertainty and instill clearer direction with immediate action.

100 Genius Side Hustle Ideas

Ready to escape the 9-5? The Hustle's side hustle database gives you 100 proven income opportunities, categorized by startup investment and skill level. Each idea includes real profit potential and time commitment details. Sign up now to unlock your next step to financial freedom and join our community of 1.5M entrepreneurs.

“Shams and delusions are esteemed for soundest truths, while reality is fabulous…

When we are unhurried and wise, we perceive that only great and worthy things have any permanent and absolute existence,

that petty fears and petty pleasures are but the shadow of the reality.”

-Walden by Henry David Thoreau

PARADIGM SHIFT

The Fed’s Secret Weapon

There are two main tools that the Federal Government and the Federal Reserve use to target full employment and a 2% average annual inflation rate.

Fiscal and monetary policy.

Fiscal policy is in the hands of the Congress and President. Monetary policy is in the hands of the Federal Reserve.

Fiscal policy could be the creation of government jobs (known as demand-side economics), or it could be lowering taxes and deregulating (known as supply-side economics).

Monetary policy comes in the form of buying and selling government bonds, or simply allowing them to expire.

But there’s another tool that rarely gets discussed. That is the tool of psychology.

The Fed has a slew of research and mathematical formulas in its vault about how consumer expectations play just as much a part in the health of an economy as do the Fed’s monetary actions.

In the medical field, there’s the placebo effect. In economics, there’s something very akin to this same concept. And the Fed uses it as a secret weapon to combat inflation and unemployment.

You see, the Fed operates largely based on an economic theory called Keynesianism. In Keynesianism, the intentional raising and lowering of interest rates through the purchase, sale or expiry of US Treasuries, is the method by which the Fed attempts to achieve its two mandates: full employment and low inflation.

But here’s the problem.

If they lose control of the narrative, and people begin to BELIEVE that high inflation is here to stay, then high inflation very likely will be here to stay.

Why?

Because if someone doesn’t believe a dollar today will buy as much as a dollar next year, then they will buy their good or service now instead of later. If too many people do this, the near-term increase in demand will push up the price of goods and services.

This increase in price simply confirms in the minds of more individuals that inflation is, indeed, here to stay. And contagion happens.

To fight the inflation, the Fed then has to raise interest rates higher. But if the economy starts to suffer, they have to make a choice whether to fight inflation with high interest rates or to stimulate job growth with low interest rates.

The good thing about this potential is that, so long as the money supply (M2) doesn’t accelerate too rapidly along with velocity of money, the greater demand will eventually inspire greater supply, bringing prices back to a more stable level relatively quickly.

But here’s the more dangerous scenario this time around.

If interest rates are higher than expected inflation (which right now they are!), people may slow spending and increase saving in order to guard against future economic downturns while also increasing purchasing power with guaranteed interest. This opposite action of slowing spending can induce recession!

It’s a slippery slope: too much or too little spending can lead to economic challenges. But the latter scenario, in my opinion, is more dangerous than the former at this point. Which is why I believe it’s in the Fed’s best interest to lower interest rates in this month’s meeting by 25 bps (0.25%).

Have you heard the Fed use the word “transitory” with regard to inflation? Part of the fight against inflation is monetary policy; the other part is the attempt at self-fulfilled prophecy. That’s done by a careful selection of words to set widespread expectations, therefore affecting everyday consumer activity.

They have to choose their words carefully so as not to imply that they are accelerating their planned interest rate cuts, which could increase concern about inflation.

So what is our best course of action in this big picture?

What can we personally do?

It’s very simple. Here’s the answer:

Don’t make buying decisions based on fear.

In other words, don’t change how you spend your money because you’re afraid of an unknown future.

Money is money. It might be worth 3% less or 5% less a year from now. But there’s no limit to what you personally can be worth in earning potential a year from now. And that comes, not from over-saving greedily or overspending fearfully, but by establishing regular habits that improve your education, experience and ability to add value to a company (even your own!).

That will have a much higher return on investment for you, and a much better impact on society more generally, than trying to save or spend to fare just a smidge better in difficult economic times.

An emergency fund is a must. This covers 3-6 months of living expenses. But this should always be a part of someone’s financial plan, not just when the economy starts to get shaky.

Fortunately, the Federal Reserve has shown that even with all the talk about tariffs, the Survey of Consumer Expectations from February shows that 3- and 5-year expectations for future inflation have remained unchanged at 3%.

Stocks typically weight the next 3 to 30 months most heavily when determining a present value. If 3-year inflation remains unchanged, even with all the new tariffs, then the main threat of recession comes not necessarily from expected inflation but from the Federal Reserve making a mistake in its choice of keeping interest rates too high for too long.

FINANCIAL TOOL

Treasury Inflation Protected Securities (TIPS)

There are plenty of ways to stay ahead of inflation over the long run. Some work best in the short-term. Others are more effective over the long-term.

As with virtually all things investment-related:

More short-term risk = more long-term potential reward

Less short-term risk = less long-term potential reward

Treasury Inflation Protected Securities fall under the latter. These are very high-quality investments, backed by the full faith and credit of the US government.

They won’t make you rich, but they will generally keep your money from losing purchasing power.

Here’s how they benefit you.

The principal value of TIPS adjusts with the Consumer Price Index (CPI), increasing with inflation. They are issued in 5-year, 10-year and 30-year increments. But don’t forget that you can buy them for about any timeframe in-between in the secondary market.

In addition to keeping pace with inflation, they also make semi-annual interest payments to you—a fixed percentage of the inflation-adjusted principal value.

At maturity, the owner is repaid the higher of 1.) the principal value (adjusted upward if inflation has occurred) or 2.) the face value at which the TIPS were first issued.

Here’s an example of this in action.

Imagine a TIPS which you bought for $100, but inflation of 10% has taken place over the last two years according to the CPI. Now the adjusted principal of the TIPS is $110 ($100 × 1.10). If it was paying a 3% interest rate on $100 at the beginning, it is now paying 3% on $110, so the dollar amount of your interest payments has also increased.

The benefit that TIPS have over other types of bonds is that other bonds don’t necessarily keep up with inflation, especially if inflation starts to accelerate unexpectedly.

The risks of TIPS are these:

In rare cases of deflation, the principal of TIPS may decrease, reducing future interest payments. At maturity, however, TIPS will pay at least the original face value.

They pay lower interest than other types of Treasuries because of their added benefit of a rising principal value based on CPI. Return equals interest plus rising principal.

Like other bonds, TIPS can lose market value if interest rates rise, meaning you may receive less than face value if selling before maturity.

Why own TIPS?

If you have a short-term goal for the money in the next 1-5 years, holding a TIPS to maturity over that time period can help protect against loss of purchasing power.

If you simply want to maintain purchasing power over any time period, without the need or desire to make beyond that.

If you want to reduce overall volatility of a larger portfolio that includes more risky assets (such as stocks).

If you want greater likelihood of earning higher than a money market account rate at the bank over time for a portion of your savings, such as a part of your emergency fund or your occasional expense fund.

HERE’S HOW I CAN HELP

Launch Your Personal Wealth Expedition!

Ready to take control of your financial destiny?

Here are the two foundational courses which will set you on course to radically transform the way you live and work.

Budget, Build, Bridge: The Roadmap to Financial Independence

This course will lead you step-by-step toward developing your escape plan into a life of comprehensive wealth: time, flexibility, purpose and money.

Each lesson builds upon the last, covering these main topics:

Master high-impact budgeting techniques to create a surplus today.

Develop a plan to become debt-free in record time.

Raise your salary this year.

Use tax strategy to fast-track your goals.

Bridge your way to entrepreneurship.

Advanced Investing for Financial Freedom

Whether you're new to investing or a seasoned expert, this course is designed to make anyone a master of what I believe to be the most important investing concepts.

Here's what you'll learn in this course.

The foundational concepts for analyzing the risk and performance of mutual funds and ETFs.

How your goals affect the allocation of your investment portfolio.

How to fine tune the risk factors in your portfolio to weight the odds of success in your favor.

How to identify stages of the market cycle and build your portfolio around it.

How, when and why to hedge against downside risk.

How this all ties together as one comprehensive wealth expedition from ground zero to financial independence.

With investing, it often takes an understanding of just a handful of concepts to make all the difference in your ability to make tremendous wealth over time.

My goal with this course is to offer you what I see as the most important concepts to successful investing, setting you on course to achieve your dream life well in advance of retirement age using simple but powerful habits of finance.

How did you like today's newsletter?I'm always looking for ways to offer greater value to fellow explorers. Your feedback helps set the direction for future content! |

I’d love to hear from you. Let me know what you’d like to see in upcoming newsletters, articles, or a digital course at Contact Us - The Wealth Expedition.